A Deep Dive into Paytm

A Deep Dive into Paytm

The history, business models and financials of an iconic Indian startup

For a summary of the article, click here. At some point, I will also be releasing a follow-up, which will cover competitive analysis and a deeper look at some of their individual business lines.

Introduction

Here’s a staggering statistic - in 2013, all digital transactions in India were approximately 85,000 crores ($15 Billion).

In December 2021, UPI alone ( a new payments rail) did $110 Billion. In other words, UPI does more now in a week than the entire country did less than a decade ago.

There are five factors responsible for the incredible growth of Indian digital payments. Demonetization & COVID created incentives for the population. UPI & Jio (the telecom company that brought dirt-cheap internet to the masses) created the infrastructure. Paytm sowed the seeds by teaching hundreds of millions of Indians, many of them illiterate, to use their phone for payments.

Despite all this, Paytm’s journey has only just begun. Paytm’s vision for success involves providing financial services to half a billion Indians. If they succeed, they would have transformed India again.

They also need to transform their balance sheet. After over a decade of operations, they still reported a loss of nearly 680 Crore ($64M) last quarter. In November, they went public in a much-maligned IPO, seeing their market cap halved from nearly $20 Billion to about $10 Billion as of writing. The past few years have been encouraging, as the company became a lot more efficient in driving growth. However, much still needs to be done.

Critics think Paytm’s founder, Vijay Shekhar Sharma, is a typical overzealous tech CEO who uses grand promises of changing the world to hide a flawed business model. But after watching multiple interviews and investor calls, I think Sharma’s passion for democratization is genuine, and like any founder-led company, it may be percolating down the hierarchy. After poring through their reports, I’m convinced that the business model is solid. Remember this is a company that has Berkshire Hathway on the cap table- the same Berkshire Hathaway that has largely stayed away from private tech companies.

Whether it’s worth $10 Billion, let alone the $20 Billion it went public at that’s another question altogether.

An Overview of Paytm’s Business Model

Paytm’s goal is to embed itself in as many financial transactions as possible, and charge a take rate where it can. But this is low-margin revenue that will never justify Paytm’s lofty valuation. Paytm’s true potential will come from finding other ways to monetize its ecosystem- through lending, advertising, insurance, wealth management, etc.

To better understand Paytm’s place in India’s crowded payments ecosystem- it’s best to see the evolution of the product and the fintech ecosystem.

First Era of Fintech

The first era of Indian Digital Payments started in the late 2000s. Mobile recharges were the initial use case but soon expanded to e-commerce, online wallets, bill payments, and ticketing. With over a hundred million users, Paytm comfortably won this era. Its wallet was a key payment method with leading digital platforms like Uber and Indian Railways. Paytm-branded QR codes became common across small stores and street vendors in big cities. In 2015, its travel platform alone crossed $500M in GMV.

Nevertheless, this era was limited to a small set of use cases amongst the affluent population. The total amount of transactions through these new platforms was probably less than $20 billion annually, and India’s fintech ecosystem resembled a small pond.

2016- The turning point

In Nov 2016, Paytm got a gift beyond their wildest dreams. In a move known as Demonization, all existing cash was rendered obsolete, and everyone was required to exchange their existing currency with new ones at their bank.

This led to a massive cash shortage in the short term and boosted digital payments. Paytm took full advantage, and as the pond of the digital payments ecosystem became a lake, it established itself as the biggest fish. Growing in ambitions, it began churning out new initiatives, such as Paytm Mall- an e-commerce platform. In 2017, it would also receive a banking license from RBI (India’s Central Bank), albeit a limited one with severe restrictions on operations.

2016 was also the first full year of operations for Jio, a telecom network offering 1 GB a day for less than $1 a month. Other telecom operators responded by reciprocating. Using low-cost Chinese smartphones that were widely available, hundreds of millions of Indians now had continuous internet access.

The stage was set for UPI- a payment rails through which anyone could transfer funds directly to a bank account using a smartphone, without being charged a cent. It spread like wildfire, its already monstrous growth was supercharged by COVID.

Source: Bernstein’s Pre-IPO report on Paytm. UPI figures on the graph on the right, others on the left.

However, even as UPI turned the lake into an ocean, it also introduced far more dangerous competitors with much deeper pockets. Whereas the Paytm interface was crowded with its numerous use cases, Google and Flipkart* owned PhonePe shot ahead of Paytm with a clean UI dedicated to a single purpose- UPI Payments. As of 2021, Paytm was a distant third in the market.

However, if we dig deeper into the UPI value chain, we find that Paytm is actually in a very strong position.

*Flipkart was the Indian version of Amazon that was acquired by Walmart for $16 Billion.

How UPI works

A UPI transaction takes seconds. You open your UPI app, put in a phone number or scan a QR code, enter your pin, and instantly transfer money from your bank account to the beneficiary account.

A highly simplified view of this involves:

The third-party apps.

Two bank accounts.

NPCI- an Indian government organization that acts as a trusted switch.

Crucially, UPI is interoperable and works across multiple apps.

In the transaction, the UPI apps act as the bank's front-end. Even though banks do most of the heavy lifting, the UPI apps own the customer relationship. In the future, the apps will attempt to monetize by using this relationship to sell other products.

However, the banks are not quite dumb pipes- they get valuable transaction data, which theoretically, they could use to build customer profiles and credit scores. (This is important- this lack of transaction data is a major reason a majority of the Indian population lacks access to credit and other services).

As a consumer application and a bank, Paytm is the ecosystem's only player owning both the customer relationship and the transaction data. Flipkart and Google, on the other hand, need the bank's consent for using the data, and even if they get it, risk facing potential regulatory action.

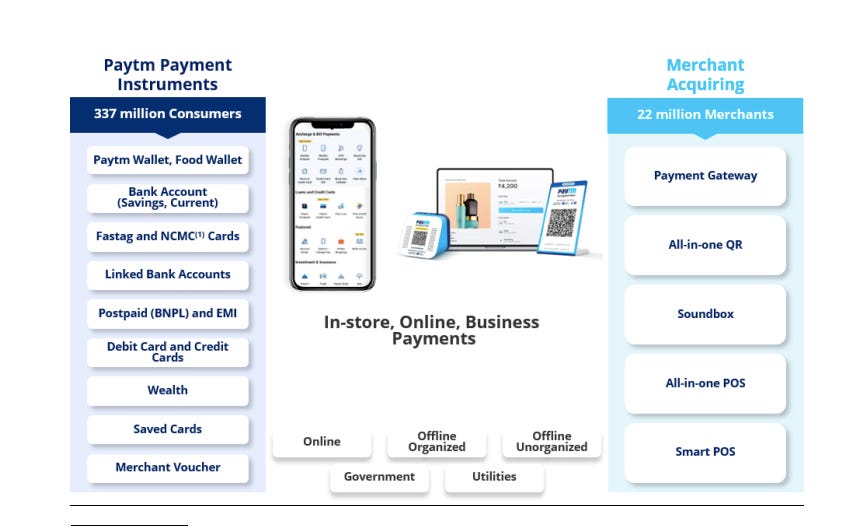

Paytm’s Merchant Strategy

The other important thing to know about Paytm's position is that it is third on all UPI transactions. However, over 80% of UPI transactions are Peer-to-Peer, while the real value lies in Peer-to-Merchant payments. Paytm realized this early, and thanks to its brilliant merchant strategy, is one of the market leaders.

In India, high-end retailers have been offering digital payments for ages. However, local mom-and-pop 'Kirana' stores still dominate retail. All UPI players understood that these were key to unlocking growth. But Paytm had been building a presence among them long before Google Pay and Phone Pe were around. Where Google Pay and Phone Pe merely focussed on onboarding and distributing branded QR codes, Paytm offered multiple products to merchants, including:

All-in-one-QR Code for all merchants: In addition to allowing payments by UPI, customers use the same QR code to pay via Paytm’s other instruments like Wallet and Postpaid. By itself, this generates no revenue as Paytm doesn't charge merchants below a certain size. But driving adoption for these instruments will enable monetization later when used at larger merchants.

SoundBox: My favorite Paytm product- a quintessentially Indian invention. Kirana stores are often short-handed and busy, and checking your phone to see the receipt of payments was cumbersome. To solve this, Paytm put the QR code on a speaker that announces whenever a payment is received (watch the video below to learn more). Impressively, Paytm charges a monthly subscription fee of $2 for it, which may not sound like much unless you’re Indian and know just how difficult it is to get your neighborhood store to spend even a cent.

POS Device: These accept payments via cards, Paytm Wallet, postpaid, etc. Paytm charges a 1-2% take rate in addition to a value-added fee, and makes about $30 a month from the average merchant, according to Bernstein.

Payment Gateways: This is used by the country's largest digital platforms, including Flipkart, IRCTC, and food-delivery giants Swiggy and Zomato. Once again, Paytm charges a small cut out of every transaction.

As of now, only Payment Gateways generate substantial revenue. The goal of the POS device and the voice box is to lock in the merchant and generate transaction data, which can then be used to offer credit products.

As someone who has run an SMB in India, I cannot stress how important credit is and how challenging it is to access. Paytm’s offerings could enable the survival and prosperity of millions of small merchants. Paytm’s merchant lock-in also makes them a potential go-to-market for other products looking to cater to India’s SMBs.

Tying it all together

The graphic below summarizes Paytm's payment offerings.

To restate, Paytm’s goal is to embed itself inside every financial transaction. A majority of its revenue comes from charging a take rate on some of these transactions. We shall refer to this as the ‘core business.’

Future Revenue Drivers

The key growth drivers called out by Paytm are lending and advertising.

The lending product has three main components- BNPL (Buy now, Pay Later), Personal Loans, and Merchant Loans. Paytm's limited banking license doesn't allow lending from its balance sheet. However, the quality of its partners- such as HDFC and Aditya Birla Finance- is a strong signal about the power of its consumer base and transaction data. If Paytm’s bid to become a full-fledged bank is successful, then both the value (and the risk) of the lending business may increase tremendously.

Advertising and Paytm, on the other hand, are seemingly strange bedfellows. After all, increasing advertising inventory hurts the user experience, and Paytm’s user lock is much weaker than that of Google or Amazon. But if Paytm can strike that balance, advertising has potential. It has tons of transactions data, over a hundred Million KYCed customers, native e-commerce and ticketing, and the ability for merchants to make ‘mini-apps’ inside Paytm.

The real constraint may come down to ad inventory. Paytm’s main play here is 'DSP'- or Demand Side Platform, for reaching audiences outside its main app- primarily on OTT platforms for now. While the advertising business should grow several times its current number as it stands, I see its true potential being dependant upon the expansion of Paytm DSP.

There are other businesses Paytm has- most notably insurance and wealth. However, its contribution to the bottom line is limited and they have been left out of my current analysis.

Business Metrics

Before we dive deeper into specific subjects, here's a quick overview of the financials. This is how Paytm officially presents it, which I don’t find very helpful:

I've modified their reporting into something that might be more helpful for you to understand the business.

Growth and Monetization of Core Business

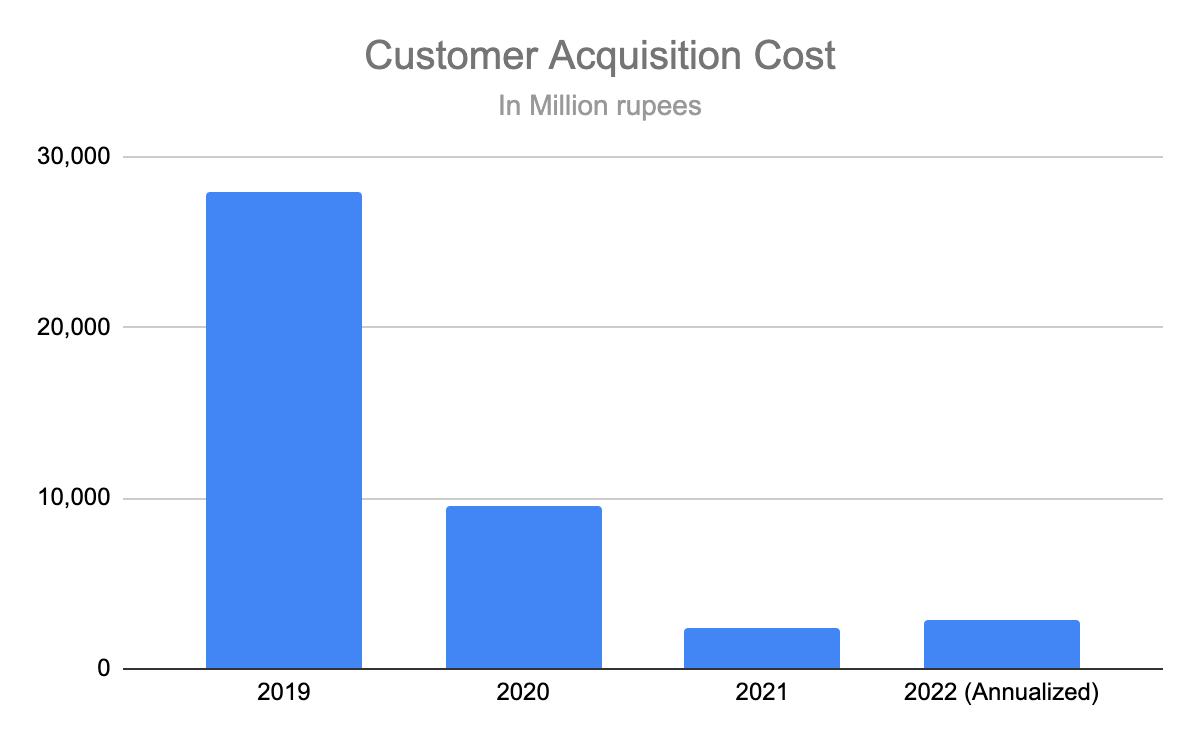

Despite all its focus on merchants- consumers remain crucial for Paytm. Like every consumer business- the company needs to grow fast at a reasonable customer acquisition cost. So how does Paytm do here?

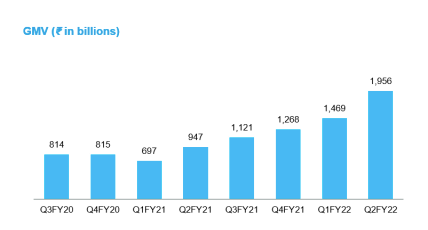

The recent metrics look fantastic- users are growing and spending more on the platform, while customer acquisition costs have decreased dramatically.

Regarding monetization, Paytm gives us a take rate figure- but defines it by dividing total revenue by GMV. I don’t find that useful- lending and advertising businesses aren’t included in the GMV. To gather the true take rate, we can instead divide revenue from core businesses (payments + commerce) by GMV and then track its progress over time.

Take rates have decreased over the year and a half. However, there isn't necessarily any cause for concern- UPI GMV (which cannot be monetized) is growing faster than overall GMV- which would lead to declining take rates overall.

Unfortunately, Paytm doesn't break apart UPI and non-UPI GMV. However, we can get a clue from their announcement last quarter that non-UPI GMV had increased 52% y-o-y. Since payments revenue increased 60% over the same period- it indicates that Paytm’s ability to monetize its payment business is actually improving. Plus, overall payment revenues are increasing significantly.

Financial Services

Paytm hasn't revealed a take rate for their lending business, but we can calculate this from their Q2-2022 results and two statements made by the managements

#1- All three parts of the lending business have a similar take rate.

#2- The lending business comprises the majority of the line item' Financial Services and Others.

Correlating the increase in lending volume with an increase in financial services revenue, we see that the lending take rate is around 5%. The complete methodology for the calculation is here.

Costs

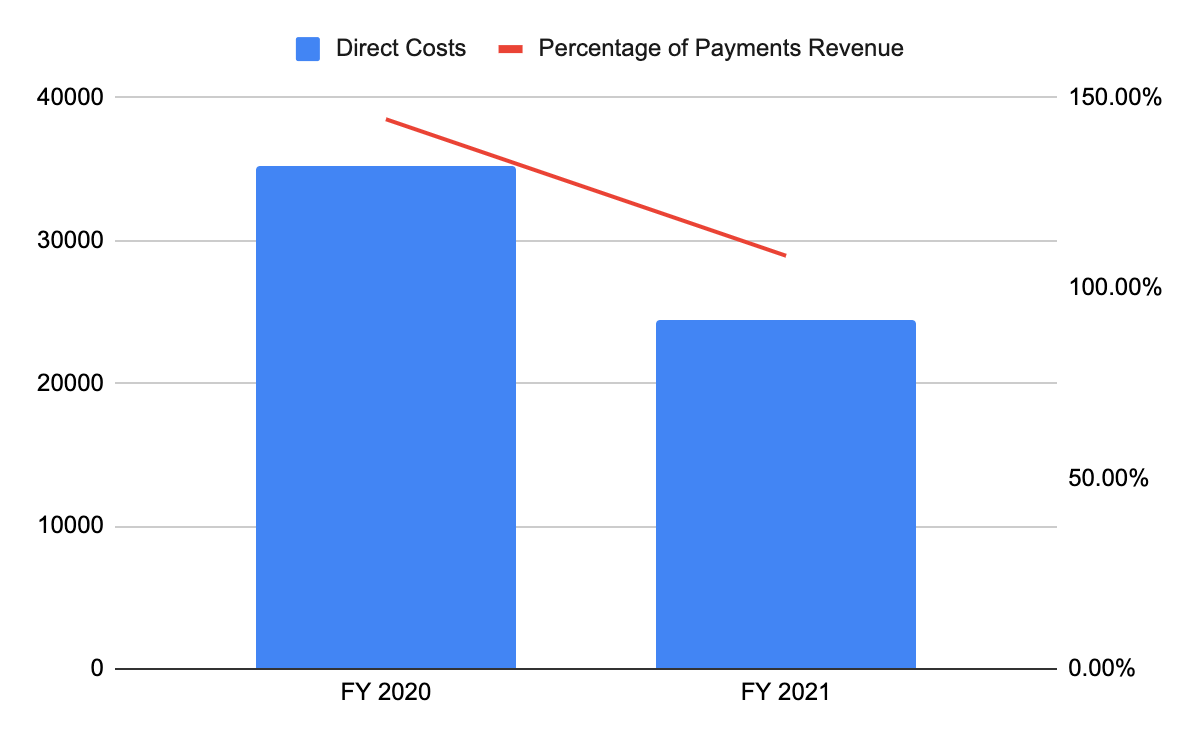

Expenses as a percentage of revenue have come down drastically, mostly driven by a decrease in marketing costs.

To understand whether the core business has leverage- we can modify what Paytm calls 'contribution margin', calculated as total revenue subtracted by ‘direct costs’ (that scale with its income). 80% of these direct costs are payment processing charges that should incur only on the core business. An additional 10% are consumer marketing costs- which the management has repeatedly stated are incurred primarily on payments revenue. This tells me that we can instead use Paytm's 'Direct Costs' to calculate the profitability of their payments revenue.

Doing this, we find that costs have declined dramatically, both as a percentage and on an absolute basis.

Tracking on Q-o-Q trends, we see that the business broke even last quarter before a sudden increase. We saw a similar increase in Q2 of last year, which is probably related to the festive season.

Summary

Paytm has a long way to go to justify its valuation. However, in the last few years, it has taken some giant steps towards getting there. Even as GMV and consumers have grown, costs have been reduced significantly. Overall costs still outpace its revenue by 50%, but it has come down from over a 100% just a few years ago.

Projecting Paytm’s Future Revenues

Warning- This part is just me having a little fun, and should not be relied upon for making investments!

I made a model to predict the 2026 EBITDA for Paytm (play around it with directly on google sheets here). It happens to differ significantly from expectations of brokerages (such as this)- who predict an EBITDA breakeven by 2027. My model and assumptions, on the other hand, predict an EBITDA of $0.5 Billion by 2026. I believe the key differences lie in our assumption for growth- most brokerages assume that heavy marketing expenditures will fund GMV growth. I think Paytm has proved that it can grow without resorting to huge losses.

I can understand the market’s skeptical response to Paytm. There is a lot of execution risk here- especially in growing a lending business to nearly an order of magnitude. Paytm also doesn’t release enough data, at least publically, to convince us otherwise.

Conclusion

All this aside Paytm is an utterly fascinating business. There are only a handful of companies around the world that single-handily changed the behavior of hundreds of millions of people. I believe that in this decade, we will see more second-order effects of that change.

One such second-order effect may be the democratization of financial services in India. The impact of providing credit, insurance, and investment opportunities to half a billion people is hard to overstate. If Paytm can execute on its achievement, its previous achievements will look small by comparison.

Excellent breakdown Fateh, I will have to do a deeper dive into paytm now.

Hey, I thoroughly enjoyed reading this. Really great breakdown of the business model and financials. Looking forward to more stuff like this from you.