The Paytm Deep Dive: A summary

I recently wrote a Deep Dive on Paytm. Since many complained about the length of the post I made this quick summary.

The growth of Digital Payments in India has been staggering, to say the least.

There are five factors responsible for this growth:

Demonetization and COVID create incentives for the population

UPI (payment rails) and a Jio (a low-cost telecom provider) created the infrastructure

Paytm teaching millions of Indians how to use QR codes for payments

UPI dominates digital transactions and is completely free for all parties to use. That means all players in the ecosystem need to find other ways to monetize.

Source: Bernstein’s Pre-IPO report on Paytm. UPI figures on the graph on the right, others on the left. Paytm’s goal is to embed itself in as many financial transactions as possible and charge a take rate where it can. However, this usually yields low margin revenues. Paytm’s true potential will come from finding other ways to monetize its ecosystem- through lending, advertising, insurance, wealth management, etc.

Paytm is set apart by its strength in P2M transactions. Its merchant strategy has been particularly good. Other vendors (GPay, PhonePay) have limited themselves to onboarding merchants onto their platform and pasting QR codes. Paytm has also provided additional devices that solve customer problems- such as a Voice Box (removes the friction of checking your phone for a payment), and a POS device. This has made Paytm the default choice for merchants with its devices, whose number has been increasing considerably.

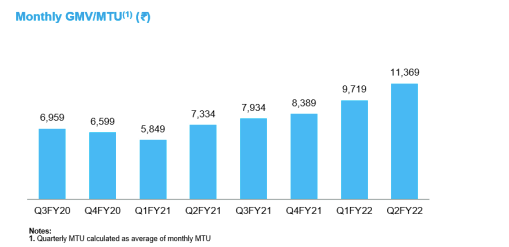

Consumer growth has been very impressive- both in # of users and transactions per user

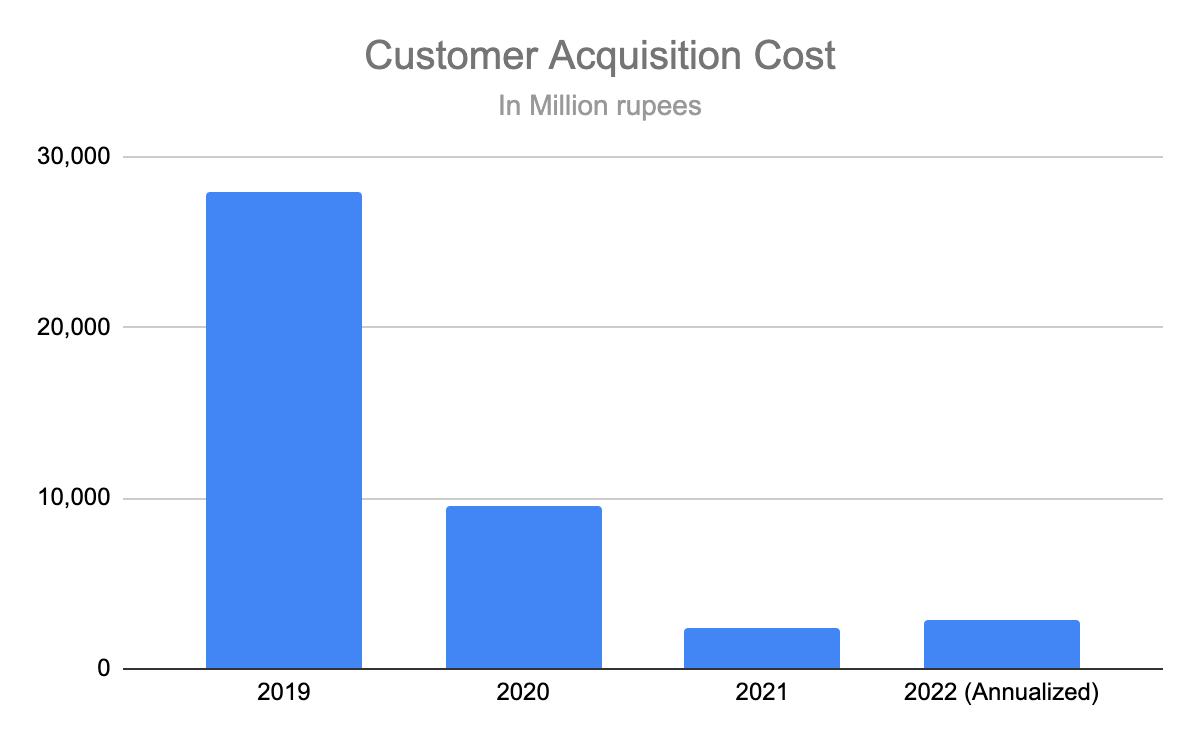

Impressively, this growth has come despite a significant reduction in marketing costs

Let’s take a quick look at their revenue and costs. I’ve modified it to fit into buckets that I find easier to understand

Core Payments Revenue:

Taking a small take (1-2%) rate of transactions through its payment wallets (for merchants above a certain size), payment gateways, and bill payments

Approximately 5% of payments made on commerce transactions (ticketing, e-commerce) made through its platform

We can use what Paytm reports as direct costs to calculate the profitability of the payment business. We find that costs have come down dramatically, but it is far from profitable

Financial Services Revenue a majority of this comes from Lending. Here- Paytm has three products, Paytm Postpaid (BNPL), Merchant Loans, and Personal Loans.

Paytm does not lend its balance sheet, and instead, partners with some of India’s leading financial institutes. Its an asset here is its transaction data- allowing credit profiling, and its access to consumers and merchants.

It appears that Paytm makes 5% of its lending volume. This is also a highly profitable business, and growing rapidly.

While Paytm offers insurance and investing as well at a significant scale- these aren’t making much revenue yet.

Others Revenue: is currently dominated by advertising. Paytm’s asset here is its base of 100 million bases KYC’d customers, its knowledge of customer transactions, and the fact that it offers native commerce on the platform.

Crucial for Paytm’s future advertising success is its Paytm DSP- where it increases advertising inventory by integrating with third-party platforms (currently limited to OTT’s), similar to Google’s Adsense

Expenses as a percentage of revenue have come down drastically, mostly driven by a decrease in marketing costs. However, the company has a long way to go to achieve profitability.

I made a model predicting Paytm’s revenue and EBITDA in 2026. You can play around it with directly on google sheets here.